Ball-Parking

7 August 2009The character is drawn about

At 14% of Earth's gravity, gravitational acceleration on Titan would be at about

That all means that he hits the ground at about

The character is drawn about

At 14% of Earth's gravity, gravitational acceleration on Titan would be at about

That all means that he hits the ground at about

The Woman of Interest draws my attention to

Telephone Terrorist: Outing an Online Outlawfrom the Smoking Gun

At 4:15 AM on a recent Tuesday, on a quiet, darkened street in Windsor, Ontario, a man was wrapping up another long day tormenting and terrorizing strangers on the telephone.

[…]

Working from a sparsely furnished two-bedroom apartment in a ramshackle building a block from the Detroit River, the man, nicknamedDex, heads a network of so-called pranksters who have spent more than a year engaged in an orgy of criminal activity — vandalism, threats, harassment, impersonation, hacking, and other assorted felonies and misdemeanors — targeting U.S. businesses and residents.

[…]

But a seven-week investigation by The Smoking Gun has begun to unravelDex's organization and chronicle the sprawl of its criminality. The TSG probe has also stripped Pranknet's leader and some of his cohorts of their anonymity, which will likely come as welcome news to the numerous law enforcement agencies, including the FBI, probing the group's activities.

[…]

With the case now moving outside the country, [Manchester, NH, Detective Peter] Marr contacted federal prosecutors for guidance. However, as Marr wrote in a May 6 report,It was obvious to me that the US Attorney's didn't have much interest in the case when I told them that the IP address of the suspectwas in Canada. In shutting the case, Marr noted,At this time I have exhausted all leads and am closing the case due to not having the jurisdiction to continue further.

If you're actually trying to install another version of Firefox, then click on the Firefox

tag, as there may be an entry on that other version.

Firefox 3.5.2 has been released. I imagine that someone will soon provide an .rpm; but, for now, Red Hat users will have to install things from a tarball. Since a fair number of the hits to this 'blog are from searches as to how to install Firefox 3.0 under RHEL 5.x, I'm going to infer that people are and will be surfing the WWWeb for instructions on how to install Firefox 3.5 under RHEL 5.x.

My first piece of advice is that one not install Firefox 3.5.1. When I tried using it, it would do something that caused the Linux user account to be logged-out. However, I've being trying version 3.5.2, and so far I've not had that problem with it. [Up-Date (2009:08/17): Unfortunately, I have since had some problems with version 3.5.2 logging me out of the system, and on one occasion it screw-up the display resolution. But these problems have not been so frequent as to move me to stop using this version.] That said, here are the steps that I recommend:

firefox, which should be dropped-in as a sub-directory of something. If you want to ponder where, then study the FHS. As for me, as root, I put it in /opt: tar -xjvf firefox-3.5.n.tar.bz2 -C /opt/nwith the actual number from the archive that you downloaded.)

compat-libstdc++-33 (a Gnome C++ compatibility library): rpm -qa | grep compat-libstdc++-33yum install compat-libstdc++-33chcon -t textrel_shlib_t /opt/firefox/libxul.so/opt, or renamed the firefox directory, then you'll need to modify the above final argument to chcon accordingly.).desktop file for Firefox (though you may already have one). As root, edit/create /usr/share/applications/firefox.desktop, ensuring that it reads(Again, if you didn't install in[Desktop Entry] Categories=Application;Network;X-Red-Hat-Base; Type=Application Encoding=UTF-8 Name=Firefox Comment='WWW browser' Exec='/opt/firefox/firefox' Icon='/opt/firefox/icons/mozicon128.png' Terminal=false

/opt, or changed the name of the firefox directory, then you'll need to change the above accordingly.)SEC Charges Bank of America for Failing to Disclose Merrill Lynch Bonus Paymentsfrom the SEC

The Securities and Exchange Commission today charged Bank of America Corporation for misleading investors about billions of dollars in bonuses that were being paid to Merrill Lynch & Co. executives at the time of its acquisition of the firm. Bank of America agreed to settle the SEC's charges and pay a penalty of $33 million.

The SEC alleges that in proxy materials soliciting the votes of shareholders on the proposed acquisition of Merrill, Bank of America stated that Merrill had agreed that it would not pay year-end performance bonuses or other discretionary compensation to its executives prior to the closing of the merger without Bank of America's consent. In fact, Bank of America had already contractually authorized Merrill to pay up to $5.8 billion in discretionary bonuses to Merrill executives for 2008. According to the SEC's complaint, the disclosures in the proxy statement were rendered materially false and misleading by the existence of the prior undisclosed agreement allowing Merrill to pay billions of dollars in bonuses for 2008.

So, the SEC asserts that the officers of Bank of America stole about $5.8 billion from their stock-holders, but has agreed to settle the case in exchange for $33 million from, uhm, the stock-holders.

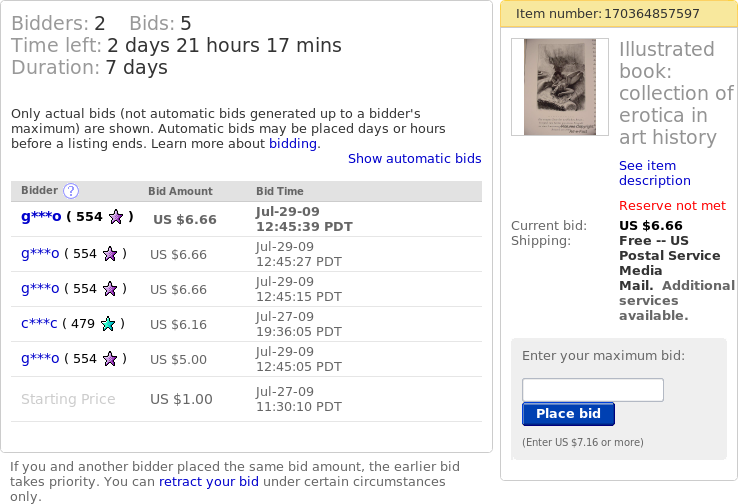

I am amused by this eBay bid history:

I'll translate:

reserveprice.

maximumbid of $6.16; this does not meet

reserveprice, so first bid is $1.00.

maximumbid of $5.00; entry automatically pushes bid of first bidder to $5.50.

maximumbid more than 50¢ than first bidder's

maximumbid, and finds that his or her bid is now $6.66.

maximumbid, but his or her bid remains $6.66.

maximumbid, but his or her bid remains $6.66.

If the second bidder were to enter a bid not less than the seller's reserve

price, then his or her bid would become that. Otherwise, his or her bid will remain at $6.66 until some other bidder enters at least $7.16.

(BtW, I put the words reserve

and maximum

in quotes, because, as far as I'm concerned, eBay abuses each term, one way or another.)

Senate group omitting Dem health goalsby David Espo of the AP

Like bills drafted by Democrats, the proposal under discussion by six members on the Senate Finance Committee would bar insurance companies from denying coverage to any applicant. Nor could insurers charge higher premiums on the basis of pre-existing medical conditions.

[…]

Individuals would have a mandate to buy affordable insurance, but companies would not have a requirement to offer it.

Let's walk through what it would mean if insurers could not deny coverage to any applicant and could not charge higher premiums on the basis of preëxisting medical conditions.

The out-lays of insurers would of course increase, so the they will do one and likely both of two things:

In the absence of requiring people to purchase coverage, fewer people would buy insurance voluntarily. Those most likely to reduce their demand for insurance would be the less affluent and those who perceived themselves as relatively healthy. A significant share of the latter would indeed be relatively healthy, and their departure would mean that the average out-lay per subscriber would increase, which would push-up costs. The departure of the less affluent would tend to push-down out-lays, as the less affluent tend to lead less healthy life-styles, but it would be unreasonable to expect the less affluent to depart in sufficient numbers to restore the lower price, and I'm not aware of anyone advocating a strategy of pricing the poor out of the insurance market.

In fact, without compulsory subscription, it becomes less reasonable to subscribe until one actually needs treatment. Coverage would no longer function as insurance because it needn't be purchased on a precautionary basis. Instead, subscription would simply be a buy-in for some programme of medical care. When the expected cost of needed medical care were less than the buy-in price, one should not purchase a subscription; when the expected cost of needed care were greater, one should buy a subscription.

The proposal is to make subscription compulsory, in which case it's not clear why insurance companies should continue to be involved at all. Insurance premiums would have been replaced with a tax (regardless of whether it were called a tax or called a user fee or called a premium), and the insurance companies would be functioning as extensions of the state. Possibly a bona fide insurance could be offered to supplement coverage provided under the proposal, but it remains none-the-less unclear what legitimate reason there might be for using insurance companies to collecting a tax or to reïmburse those who provided state-mandated coverage. I'm inclined to interpret the intent in part to be to buy-off the insurance companies, giving them what will seem a guaranteed source of revenue, and in part to give a private-sector façade to a state monopsony.

Returning to the issue of the increase in buck-per-bang price, a consequence is going to be that most people who would insure in the absence of the proposed measures are going to have less coverage in their presence, unless they are required to have as much or more coverage than before, at the greater prices implied by not imposing higher fees on those with preëxisting conditions.

After some vacillation over the question of to which of two journals next to submit my paper, I have submitted it to a game theory journal which has published at least one other article attempting to operationalize incomplete preferences. (I think that attempt rather less satisfactory than mine.)

I have, alternately, been considering submitting to an older journal, based in Europe, which focusses primarily on mathematical microëconomic theory, but I decided both that they would be more likely to reject the paper as too specialized, and that my paper would be less widely read if published there.

Too Specialized

Good L_rd! In response to my submission, the editor of the third journal responded

While I find the paper interesting, I feel it is too specialized a topic for a general audience journal such as [ours].

The thing is that, unlike the previous two journals, which cover economics in general, this is a journal of microëconomics. Yet, like the editor of the previous journal, the editor still feels that the paper is too specialized for the audience. (Though, as noted, this third journal was recommended by that editor of the second.)

I need to figure-out just who won't think it too specialized.

I stopped actively collecting comic books in my very late teens. But I held onto my collection, and hope to keep it to the end of my life. And for many years it had a gap in it that greatly annoyed me; specifically, I needed Giant-Sized Conan #3, in mint condition, to plug a hole. Whenever I would go into comic book stores, and the couple of times that I went to San Diego Comic-Con, I would look for that specific issue, in that condition. A few weeks ago, I finally managed to obtain a copy.

At the end of April of last year, I announced

I have secured at least one complete exemplar of every variety of [working Mannheim slide-rule tie-clips] that was made for resale.

but retracted that claim about a week later. I am going to be so bold as to make the claim again. Actually, I obtained an exemplar of the missing sort some time ago, but its indicator wasn't in the best condition. The exemplar that arrived to-day was as-new, in its original box (whose exterior is a bit abraded) and with its original instructions (as-new).

I'm not sure how to count the sorts of clips in this collection, as there are minor variations, but I'd say that I have thirteen or fourteen sorts.

I have submitted my paper to a third journal, that recommended by the editor who rejected it at the previous journal.

This third journal is one from an association which, like many, charges a lower submission fee to its members. Even with the annual dues and on the assumption that I only made one submission in a year, I would still save money, so I joined. However, after I registered and paid, I learned that it could take up to four weeks for my membership information to be recorded and provided to me. Hence, this delay between submissions. I'm not sure that the money saved was worth that delay.