A recent comment by Zenicurean notes, implicitly, that economic pædagogy often uses a widget as a hypothetical economic good.

I most frequently use the veeblefetzer (borrowed from Harvey Kurtzman) when I want a good about which the audience will know little or nothing, and the hot dog when I want a good that will seem familiar.

I like the hot dog as an example in part because it has a long tradition in economic education while being fairly absurd as an artifact.

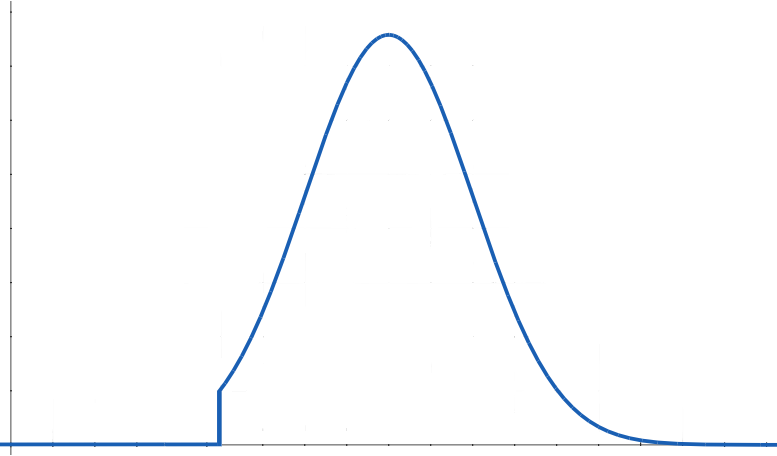

I also like it because it is easy to explain the idea of a shift in the demand curve using the hot dog. First, I present my students with a set of prices, polling them as to how many hot dogs they would buy at each of these prices; that gives us an initial demand curve. Then I discuss some of the things that are permitted to go into hot dogs, and we repeat the process for the prices. (So far, the demand curve has always shifted inwards.)

But the main reason that I like to use hypothetical hot dogs is because I think back to a question on the economics GRE when I took it.[1] In the set-up for the question, a family was working-out its annual budget, and decided that they would spend $800 per year on hot dogs, regardless of the price of hot dogs.[2]

The question was of what sort of demand elasticity were here displayed. Elasticity is a measure of sensitivity or responsiveness, with a general form of

±(%Δy / %Δx) = ±(Δy/y) / (Δx/x) = ±(Δy/Δx)·(x/y)

or of

±(dy/dx)·(x/y)

(Whether there's a negative sign and whether an instantaneous form is used is based on what's convenient and practicable.) In the case of

demand elasticity, the

y is quantity demanded, and the

x is unit price. One might think that demand responsiveness could be measured more

simply by

slope (Δ

y/Δ

x or d

y/d

x), but elasticity has a useful property. When elasticity is

less than 1 in absolute value, responsiveness is sufficiently

weak that expenditures (the product of quantity demanded and unit price)

increase as price is increased; whereäs if elasticity is

greater than 1, responsiveness is sufficiently strong that

expenditures shrink as price is increased. The seller gets

less revenue by increasing prices in the second case, where the curve is said to be elastic (sensitive); the seller gets

more revenue by increasing prices in the first case, where the curve is said to be

inelastic (

insensitive).

If the elasticity is exactly 1 (in absolute value) then quantity demanded drops or rises to exactly off-set any price change; expenditures are constant as price changes. This is called unit

elasticity. (BTW, a demand curve that is everywhere unit elastic will be a hyperbola.)

On the GRE, I was supposed to identify the demand curve of the family in the question as unit elastic, and so I did. But, because I'm not autistic, I was also greatly amused by this example. Imagine a family that is conscientious enough to budget, but they eat hot dogs. Imagine a family that budgets, but budgets such that if a hot dog costs $1600 then they will try to buy half a hot dog, and if a hot dog costs a penny then they will buy eighty thousand g_dd_mn'd hot dogs!

I laughed when I read this question. And, because I made multiple passes through the test, I glanced at that question repeatedly, laughing each time. I was the only person in room laughing. (The room had people taking different subject

GREs, and I may have been the only one taking the economics test.)

When I use hot dogs as an example, it's mostly just in fond memory of that hypothetical family, crazy for hot dogs.

[1] This tale may seem somewhat familiar to those who read my now long-since-purged LJ.

[2] The amount may have been $600 per year, or perhaps $400 per year; it has been quite some time since I took that test, and I don't remember. But, mutatis mutandis, my remarks hold.

usually doesn't make a great deal of sense, because few people will even be near the lower bound, rather than a fair number at it or just barely above it.

usually doesn't make a great deal of sense, because few people will even be near the lower bound, rather than a fair number at it or just barely above it.

![[detail of screen-capture, showing price of $4959.29]](wp-content/uploads/2011/04/NM_GEB_price.png) The lowest price that I found was four thousand, nine hundred and fifty-nine dollars, and twenty-nine cents.

The lowest price that I found was four thousand, nine hundred and fifty-nine dollars, and twenty-nine cents. ![[detail of screen-capture, showing range of prices]](wp-content/uploads/2011/04/addall_big.gif)